levoncigol/iStock through Getty Photographs

“Management your personal future or another person will.” – Jack Welch

The Previous

At numerous occasions throughout the yr, I usually return in time and try what the funding panorama appeared like and how I used to be deciphering the scene. I’ve discovered that to be fairly informative as a result of whereas the gamers have modified the patterns usually repeat.

On March 24, 2018, I penned an article with the headline:

S&P 500 Weekly Replace: A “Bottoming” Course of For Shares Or A Deeper “Correction’ Looming?”

The fairness market was within the midst of a corrective section testing help within the 2500-2600 zone, and I famous:

What we’re witnessing is a typical bottoming course of, a course of that takes time. Persistence is now required.”

Fed Chair Powell had simply raised charges by 25 foundation factors, however it was obvious the Fed posture at the moment was nothing to be involved about:

The Fed stance stays the identical, the tempo of fee will increase shall be measured and data-dependent. All of that is bullish for shares. Rates of interest at these ranges, amidst the current Fed outlook, are NOT a cause to shed fairness publicity.”

Satirically traders have been involved a few “struggle” again then as properly, however it wasn’t a ‘human tragedy”, it was a possible commerce struggle over “tariffs”. Actual GDP was reported at 3.6%, inflation was working at 2.3% and the headlines just couldn’t resist exhibiting how fuel costs might hit $3 and the way unhealthy the scenario would possibly get. In step with that thought course of, imagine it or not, analysts/economists have been working round preparing for a recession.

Most of these analysts weren’t being attentive to information. As an alternative, they have been pounding an agenda.

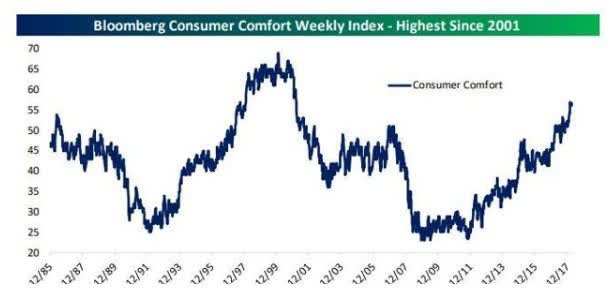

Shopper consolation is tracked utilizing responses on three classes: the financial system, the local weather for spending, and their private funds. Because the graphic illustrates, the index is at its highest degree since 2001.”

Shopper Consolation – 2018 (www.bespokepremium.com)

Households have been in nice form and amazingly there have been no stimulus checks handed out to make that occur. Customers generally is a resilient group.

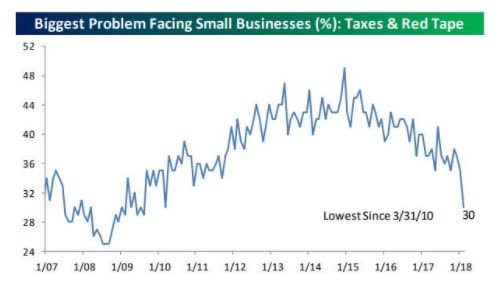

Again in October 2016, a mixed 42% of small companies cited both Taxes or Authorities Regulation as their greatest drawback, and the 2 have been tied for the lead as being cited by the most important proportion of companies.

Small Enterprise Survey – 2018 (www.bespokepremium.com)

Within the March 2018 report, the mixed studying of those two issues was simply 30%, which was the lowest in eight years.

The job image was sturdy with a 4% unemployment fee and preliminary jobless claims have been at lows final seen in 1970.

So as an alternative of listening to the info, it was all concerning the biased opinion that was preserving traders and a few cash managers scared. That turned out to be a wrong-footed strategy based mostly on emotion. I do know that to even be FACT for the reason that S&P rose from 2500 to the pre-Covid excessive of 3400.

When it got here to figuring out new tendencies in early 2018 it was my perception:

“Whereas Expertise takes a properly deserved break, Vitality and Supplies present indicators of life. Check out a few of the power explorers. The person names I am monitoring within the Savvy Investor Market service are up 13% since March twelfth. Many are additionally posting new 52-week highs.”

WTI was buying and selling at $66/barrel, and it was highlighted in a current Dallas Fed Vitality Survey that just about half of oil & fuel CEOs count on a “substantial” enhance within the variety of rigs if crude stays between $61-64 a barrel. Fairly ironic given the power disaster the financial system faces as we speak.

There was no ‘wavering’ within the bullish stance again then. As an alternative, “Conviction” was HIGH.

The secular BULL market is entrenched, the positives far outweighed the negatives however the ‘skeptics’ worry was rising rates of interest. Given the backdrop that was simply laid out, including in Company earnings development, the likelihood that shares shall be larger down the street stays excessive. Sifting via the entire rhetoric and worry based mostly reporting is not simple. Specializing in what actually issues has handled savvy traders to good rewards throughout this bull market. I do not imagine we must be making ready for the tip simply but.”

Many will not agree with me on my market stance now when the 2 dirtiest phrases at the moment are on the tip of their collective tongues, Commerce Struggle.”

Again then the recommendation was to comply with Howard Marks’ quote:

Buyers face not one, however two main dangers: the chance of shedding cash and the chance of lacking alternatives.” – Howard Marks

March 2018 was an recognized ‘alternative’.

The funding panorama has modified dramatically since then. A discernable development emerged in mid-2021. From there it began to take root, making it a really difficult time for traders. Much like 2018 the fairness markets have skilled a corrective section and launched into a “bottoming” course of. Whereas there are some financial similarities that we will look to for consolation, the similarities to then and now finish there. This altering scene has disrupted the scenario to the purpose the place an investor doubts their subsequent transfer.

Seeds have been planted final yr that at the moment are beginning to present up as points. With this “change” afoot market contributors will not have a robust footing wherein they are often certain the following step will not take them tumbling down the cliff. Going ahead this would possibly not be your typical BULL market scene the place nearly all of indicators have been pointing in the identical path. In 2018 the problems have been conjured up, exaggerated, and magnified. At the moment they’re all fairly REAL.

The Week On Wall Road

The entire main indices entered the week trying to enhance on the current beneficial properties off of the mid-March lows. The S&P 500 began buying and selling Monday on a streak that noticed beneficial properties in 7 out of the final 9 buying and selling days. A see-saw session was lastly resolved to the upside because the rally continued on Monday and the consumers stayed in management on Tuesday extending the rally to 11 days.

The S&P’s 11% rally ended on Wednesday and by the tip of the week, the index gave again 3% of that acquire. It resulted in a blended image because the S&P, NASDAQ, and Russell 2000 posted modest weekly beneficial properties whereas the DJIA and Dow Transports misplaced floor.

The primary quarter of ’22 has performed out the way in which I anticipated. Hectic, unstable, and irritating. The S&P has given traders 10+% strikes in each instructions. A 13% correction was adopted by an 11% rebound. Indecision has set in and what’s on the thoughts of many market contributors within the path of equities within the second quarter.

The Fed & The Yield Curve

The ten-year Treasury closed at 2.38% on Friday, and the yield curve has inverted because the 2-year closed at 2.44%.

An inverted yield curve displays a state of affairs wherein short-term debt devices have larger yields than long-term devices of the identical credit score danger profile.

Buyers are rightfully involved that inversions elevate the likelihood of a recession, however recession alarm bells should not begin ringing when only one a part of the yield curve inverts. As an alternative, the chances of a recession rise as an growing variety of factors within the yield curve invert. As an example, whereas 2s10s is inverted, the three-month vs 10-year curve is nowhere even near inverted (185 foundation level unfold) and was only in the near past at its steepest degree in 5 years. Traditionally talking, when just some factors of the yield curve invert, the likelihood of a recession barely will increase. It is not till nearly all of factors within the curve invert {that a} recession within the subsequent two years turns into more and more inevitable.

I will repeat what was stated final week. Is it price maintaining a tally of? Certain. Is it price making portfolio choices based mostly on it as we speak? I do not suppose so.

The Financial system

Manufacturing

The seasonally adjusted S&P International US Manufacturing Purchasing Managers’ Index posted 58.8 in March, up from 57.3 in February. The development within the well being of the US manufacturing sector was steep general and the sharpest since final September.

Dallas Fed manufacturing index fell 5.3 factors to eight.7 in March after bouncing 12 factors to 14.0 in February. The index was at 29.3 a yr in the past.

Chicago PMI jumped 6.6 factors to 62.9 in March, higher than anticipated, and unwinding quite a lot of the 8.9 level decline to 56.3 in February.

Shopper

The consumer confidence index rose for the primary time this yr gaining 1.5 factors to 107.2 in March, after sliding -5.4 factors to 105.7 in February. The index stays properly off the pre-pandemic ranges. The parts have been blended, however expectations fell to the weakest degree since February 2014.

Shopper confidence (www.conference-board.org/subjects/consumer-confidence)

The opposite financial experiences this month confirmed that Personal Income elevated by 0.5% (in-line). Private consumption disenchanted rising 0.2% (0.4% anticipated).

On the inflation entrance, the February year-over-year PCE chain value metric rose to a 40-year excessive of 6.4% from a previous excessive of 6.0%. Whereas the core measure rose to a 39-year excessive of 5.4% from a previous excessive of 5.2%

JOLTS: job openings dipped 17k to 11.2 million in February, about the identical as we noticed in January, each just below the all-time highs. The roles are there and that implies no use for any further “help” from the federal government.

Non-farm payroll report was general strong by practically each metric. Payrolls elevated 431k in March after beneficial properties of 750k in February and 504k in January. Payrolls have elevated by over 400k each month since Could as most staff have discovered their approach again to the office they left throughout the pandemic.

The International Financial system

We have mentioned the ramifications of the “struggle” on the European financial system, which has the distinct risk of inserting the EU in a recession.

They put themselves in a “field” after they drove down the street to be depending on Russian hydrocarbons. A complete ban together with a timeline to get out from below” is now below dialogue. No matter comes out of those discussions goes to be a expensive endeavor for them and it additionally has ramifications on the worth of oil.

I proceed to advise traders to tread evenly when taking a look at what is likely to be “bargains” within the international markets. Much like an funding in ANY market, your timeline is necessary.

One factor is for certain, the investing world is revolving round commodities nowadays. Commodity exporting nations are doing very properly. Canada (EWC) and Mexico (EWW) have damaged out to new highs, whereas the relative power in Australia (EWA) and Brazil (EWZ) have improved dramatically.

The EU Presents The Biggest Danger

Nonetheless, with inflation, particularly, power prices persevering with to stress economies, below any cheap state of affairs, the U.S. is healthier positioned for the financial dangers as we speak than Europe or Asia. Within the close to time period, the power disaster will trigger a client confidence disaster. That’s possible inflicting capital to movement from East to West, we have seen this already in market efficiency within the final month, and it possible continues.

I reiterate that will probably be tough for the EU to keep away from a critical downturn of their financial system. Whereas the plans to alleviate their dependence on Russia are step one, this interim/transition interval demonstrates how their power issues are simply starting. Germany is making ready their residents for natural gas rationing. Pure Gasoline Clients within the EU pay a median of 6 to7 occasions greater than what U.S. shoppers pay.

Germany’s Producer Value Index grew 25.0 % YoY in Jan 2022, in contrast with a development of 24.2 % YoY within the earlier month. That’s an all-time excessive.

Germany PPI (www.ceicdata.com/en/indicator/germany/producer-price-index-growth)

The U.S. can stand up to a recession within the EU, however it’ll certainly have an effect on the income of multinational corporations, which ultimately have an effect on our markets. Nonetheless, a dramatic slowdown within the EU does enhance the likelihood of a worldwide recession. China is in one of the best place to keep away from a recession adopted by the U.S. After that, no nation is “protected”.

The “inexperienced local weather agenda” was a failure and can proceed to take a toll. The selections that spawned this disaster are profound. Nonetheless, they’re dwarfed by the truth that the US has determined to comply with that very same path, and depart the “disaster” to “repair itself”.

China

Disappointing outcomes on the financial scene as China’s manufacturing and services activity contracted collectively for the primary time for the reason that Wuhan coronavirus outbreak.

- China’s official manufacturing buying managers’ index fell to 49.5 in March, down from 50.2 in February.

- Official non-manufacturing PMI, which measures enterprise sentiment within the companies and building sectors, fell to 48.4 from 51.6 in February.

Each at the moment are in “contraction” territory.

Ultimate learn on Manufacturing PMIs from Markit:

Eurozone – 56.5, a 14 month low

UK – 55.2, a 13 month low

China – 48.1, falls to contraction ranges

Japan – 54.1, close to highs, 14 months in enlargement territory

ASEAN – 51.7

Whereas Manufacturing knowledge slowed in March, apart from China, PMIs stay solidly in enlargement territory.

Political Scene

“Present me your price range and I will let you know what you worth”.

That was a quote from Joe Biden whereas on the 2007 marketing campaign path.

This week’s unveiling of the proposed price range from the administration signifies no change in coverage. Extra taxes and extra spending.

Taxing “Unrealized beneficial properties” is again on the desk for some people and growing the company tax fee to twenty-eight% can also be being proposed. Taxing anybody at any degree on “unrealized beneficial properties” is anti-capitalistic, anti-investment, and greater than possible unconstitutional. The sheer incontrovertible fact that it is being proposed “once more” ought to ship chills down the backbone of each capitalist within the U.S.

In whole there are 36 new taxes within the price range with 11 of them concentrating on the oil and fuel trade. The opposite 25 punish “success”. As soon as once more the message is evident. The US oil/Gasoline trade must proceed to function below an anti-business hostile setting. Backside line; the taxes will not incentivize oil corporations to “play ball” in what’s a ballpark crammed with holes and rocks.

The “spending” proposals embody extra “protection” spending and are crammed with “wish list” items which have already been proposed and failed. The excellent news is that it might seem that these proposals have little probability of being enacted. The unhealthy information continues to be the mindset that continues to point out an anti-business, anti-investment bias. On the finish of the day, it initiatives a no-growth inflationary future.

Whereas the “wealth tax” solely impacts a small variety of individuals, it additionally has NO influence on the overall tax income collected. It quantities to a “rounding” error. So its sole function is to embark on “class warfare” that displays a convoluted infantile mentality. Federal tax revenues are at report ranges and are a perform of a pro-business, low tax setting that’s left over from the pre-pandemic period. Given the excessive tax receipts mixed with inflation working sizzling and the FED embarking on a tightening cycle, elevating taxes in ANY type provides a ball and chain to development. These proposals if adopted cement the no-growth story in place. NO authorities has ever taxed its option to prosperity.

Customers are exhibiting disdain for the upper tax mindset. Through the nice Covid migration, a Strategas Analysis research discovered high-tax states skilled a 76% enhance in “outmigration” in comparison with 2019, whereas low-tax states noticed a 25% enhance from home in-migration. Earnings migration was measured in mixture {dollars} and as a proportion of a state’s revenue, with Florida the runaway winner, gaining $37 billion of recent revenue over the past two years. At $10 billion, Arizona was a distant No. 2. California and New York have been the largest losers.

Earnings

Final earnings season the discuss was about it being one of the vital necessary since we’d get clues from corporations on what the financial system appears to be like like. It is humorous, however I am studying the identical storyline concerning the upcoming season as properly. Final season was sturdy and steering didn’t disappoint. BUT, as soon as once more the buzzwords from analysts revolve round administration commentary for 2022 steering. Many imagine that would be the main driver of fairness efficiency in April/Could.

With the worldwide points magnified within the EU and elsewhere, I proceed to level out that traders is likely to be extra inclined to begin transferring extra in direction of U.S. publicity broadly.

Meals For Thought

One other senseless “out of contact with actuality” proclamation in a new study that proclaims “Wealthy” nations should cease producing Oil and fuel by 2034.

On the flip facet:

Hess CEO John Hess stated that authorities officers and traders must be extra lifelike about displacing fossil fuels and be taught from the present volatility that the world nonetheless depends on oil and fuel.

“The main focus actually must be on power safety and oil and fuel have a significant position to play within the international financial system. Oil and fuel are wanted for many years to return and the important thing problem to grease and fuel is funding.”

Jamie Dimon and other concerned corporate executives made their case for energy independence on Monday throughout a closed-door White Home assembly. T The “Marshall Plan” message:

“Give you an all-the-above American power technique that may make America power unbiased, much less dependent upon power from different locations all over the world. It is a quite simple repair.”

For some cause, “easy”, and “widespread sense” is not a part of the US power coverage. The current coverage will hold oil costs elevated at ranges that may hold power traders in revenue but additionally can have the potential to take down your entire financial system.

Sentiment

The Day by day chart of the S&P 500 (SPY)

Every week that began on a constructive observe, ended with across-the-board weak spot, as the newest rally fizzled.

S&P 500 4-1 (www.FreeStockCharts.com)

The S&P 500 sits ~ 6% off of the highs, between help and overhead resistance. The “directionless” scene is including to the indecisiveness of traders. Anybody in search of clues as to what comes subsequent from the basic backdrop may even discover the frustration ranges excessive.

Funding Backdrop – The Current

- The job market stays sturdy, unemployment is at 3.9%, and preliminary jobless claims are at historic lows.

- Family steadiness sheets are in glorious form

- The Fed is embarking on an rate of interest cycle.

- The “struggle” on everybody’s thoughts is Russia/Ukraine and it has implications that would ship the Eurozone into recession, even when it ends tomorrow.

- Shopper “consolation” and “confidence” are at multi-year lows

- Inflation is working at 7.9.

Absolutely a blended bag for traders to sift via after which make choices. Dominant funding themes all the time exist. There are, nevertheless, turning factors in funding cycles the place many market contributors have hassle recognizing the emergence of a brand new theme, as an alternative discover themselves mired in frustration on the actual time limit the place they need to be recognizing the plethora of recent alternatives.

They grow to be pissed off exactly when they need to be probably the most interested by new alternatives. The issue is that, on this section of the funding setting, we will grow to be too complacent pursuing the previous theme slightly than endorsing a brand new asset class.

It is not really easy to “change” however the lesson discovered from the final 6-9 months stays – when there’s a MATERIAL change within the panorama, now we have to vary as properly. I convey this up as a result of lately I’ve written that within the form of market setting I imagine we’re in, an open thoughts and adaptability in strategy are extra necessary than ever. An investor cannot be married to a specific narrative as a result of apart from “Vitality”, the tendencies are fleeting in what has been a directionless market since final October.

I’ve moved on to enjoying smaller tendencies and strikes, and focus much less on “the market” and extra on particular person teams and shares. How lengthy that lasts stays a query mark because the “points” dominate the scene.

The 2022 Playbook Is Open For Enterprise

Thanks for studying this evaluation. In case you loved this text thus far, this subsequent part supplies a fast style of what members of my market service obtain in DAILY updates. In case you discover these weekly articles helpful, you could need to be part of a group of SAVVY Buyers which have found “how the market works”.

March is within the books and we will name it a “rebound” month. The entire indices posted beneficial properties and that broke the two-month streak of losses for each index besides the Russell 2000.

March Outcomes

- Dow Transports +6.8%

- S&P 500 +3.7%

- NASDAQ +3.6%

- DJIA +2.4%

- Russell 2000 +1.3%

Key Market Sectors

- Vitality +8.8% – The Chief for the third straight month

- Commodities +8.1%

- Healthcare +5.3%

- Shopper Disc. +4.2%

- Expertise +3.2%

- Financials -0.47%

- Semiconductors +0.08%

- Small-cap Worth +1.4%

- Small-cap development +1.3 %

First Quarter Outcomes

- Transports -1%

- DJIA -4.4%

- S&P -4.7%

- Russell 2000 -7.7%

- NASDAQ -8.9%

Key Market Sectors

- Vitality +37.7%

- Commodities +24.8%

- Financials -1.8%

- Healthcare -2.7%

- Expertise -8.5%

- Shopper Disc. -9.5%

- Semiconductors -12.6%

- Small-cap Worth +0.2%

- Small-cap development -11.8%

It certain has been a difficult begin to 2022. We have seen the primary vital correction in over a yr. For the primary 3 months, it has been Vitality/Commodities and little else. March noticed renewed curiosity within the Dow Transports making it the BEST performing index in ’22, Nonetheless, that is not saying a lot because it ONLY misplaced 1% for the yr.

BIFURCATED MARKET

Shopper Discretionary (XLY), Healthcare (XLV), Biotechs (IBB), and Actual Property (XLRE) posted beneficial properties this week. Whereas the Vitality and Commodity commerce cooled off. On Friday, Semis and Transports bought off exhausting signaling a “development” scare. But HIGH PE development had a constructive session.

Confused? Welcome to the second quarter.

SMALL CAPS

After a horrific January, the Russell 2000 has been the steadiest of all since then. The Russell was the one main index that was constructive in February and as reported, the small caps added one other 1.2% to their acquire in March. Nonetheless, the index continues to be down 7+% for the yr.

SECTORS

ENERGY

In lower than 2 weeks the Vitality ETF (XLE) is true again as much as resistance at $78. A degree that has capped costs since 2016. This sturdy transfer is now paying homage to the rally that came about between ’04 and ’08. In that timeframe, the XLE rallied from across the $25 degree earlier than topping out at $90 proper earlier than the monetary disaster. Satirically this rally has additionally began at $25, the 2020 March lows.

I do not see any insurance policies that may materially change provide, so if demand stays as is, the worth of WTI ought to stay elevated. Vitality shares stay a BUY on ANY dip. The charts of particular person corporations are “pristine” photos of a BULLISH development. The businesses which are paying a base + variable dividend are inflation busters.

FINANCIALS

Financials (XLF) are again to “impartial” as they’re in the course of the current highs and lows. Many of the charts for a lot of particular person shares present the identical indecisive sample. New additions must be geared to names that provide a dividend. I am not within the accumulation mode however stay in a HOLDING sample.

HEALTHCARE

Healthcare is inching again to the previous highs and has moved again to ranges seen final summer time. For now, now we have a well-defined vary with the ETF nearer the highs. The group must be thought of considerably defensive as they should not be adversely affected by inflation or larger rates of interest.

Sub-sector – Biotech

Like so many different charts I reviewed this week, I observed that the Biotech ETFs IBB and XBI have damaged a short-term downtrend. Now the query is will this transfer have endurance? I’ve talked a few bottoming sample for a few month now. The long-term development line of help drawn from the lows again in 2016 acts as an necessary indicator to keep watch over. The February lows have been NOT violated this month, preserving that help in place. That will increase the likelihood of a bounce in a sector that has lagged for fairly a while now.

Each IBB and XBI posted beneficial properties of 4% this week, and the enjoyable could be beginning.

GOLD

The Gold ETF (GLD) made a run in early March, failed at resistance ($193), and stays in a sideways buying and selling vary flat for the month. My steel of alternative continues to be Uranium (URA), and that ETF posted an 8.2% acquire in March simply outpacing the indices. Gold might glitter however Uranium shines.

TECHNOLOGY

With financial development right here within the U.S. coming into query, one space that I need to proceed to have publicity to is the sector that supplied Development. Whereas it has been all about Value recently, Development did make a slight comeback in March. In a low development setting, I would slightly have publicity to an organization that’s rising at 20% versus a Worth identify rising at 2-3%.

Sub-sector – Cybersecurity

Here’s a “Theme” with tailwinds. In contrast to lots of the extra progressive, “futuristic” funding themes, Cybersecurity has a thriving market and wish proper now, whereas additionally nonetheless having development potential. Cyberwarfare has shined a highlight on Cybersecurity lately and sadly, cyber assaults are solely more likely to grow to be a fair larger risk utilized by terrorists, criminals, and sovereign powers.

The Global Cybersecurity ETF (BUG) is at the moment barely above ($31) the place it was on the finish of 2020 ($29), which means there was no progress for over a yr now. It has proven good relative power lately, although, placing in a possible double backside in January and February.

Sub-sector – Semiconductors

A 19% rally off the March lows and the sector I believed may lead your entire market again has performed simply that. The group has retraced a few of that transfer after working right into a stiff resistance degree. An ideal sector to make use of a lined name writing technique now because it appears to be like like a short-term sideways development with a “lean” to the draw back might emerge.

That coincides with my “take what the market provides you” technique.

ARK INNOVATION ETF (ARKK)

This HIGH PE, HIGH development sector of the market is yet one more space that has damaged its downtrend. Final Tuesday was the primary time since November ’21 that ARKK traded above its 50 and 200-day transferring common for your entire buying and selling day.

The ETF rallied 3.4% this week and is now up ~37% since March 14 lows. Most of the particular person names within the group even have glorious short-term danger/reward setups. Nobody is aware of how lengthy this commerce continues and I do not recommend getting married to this group until they’ve a 3-5 yr time horizon. For the energetic traders, there’s a bundle of alternatives ready for them to shake the timber and decide up the fruit.

CRYPTOCURRENCY

Crypto began the week up virtually 6% to the very best ranges for the reason that begin of the yr. The downtrend for Bitcoin that ran from November 2021 via late January 2022 has been damaged. The $44,000-$44,500 degree has acted as resistance 3 times and with BTC rallying to 46,500 earlier than pulling again that degree might now act as help.

The related ETFs – BITO and OTC:GBTC – posted beneficial properties for the week.

FINAL THOUGHT – The FUTURE

Whereas I do not profess to have the ability to forecast the longer term when the handwriting is on the chalkboard it’s important to learn it. Inflation is HIGH, Vitality prices are an enormous a part of that drawback. What’s extra worrisome – no everlasting options have been proposed to resolve the “Vitality Disaster”.

This in flip has precipitated a “Shopper confidence disaster”. Buyers mustn’t take this evenly. These kinds of structural pressures sometimes fade slowly, which might immediate the market to begin pricing in potential stagflation.

However to have stagflation, the financial system must be stagnating. Whereas there are some early indicators of a possible slowdown, there may be additionally some proof indicating the financial system can stabilize and keep in a really low development backdrop. After all, what “forces” ultimately win the tug of struggle stays to be seen. Alongside the way in which to an eventual conclusion, there may very well be many different components that come alongside to vary any perceived consequence. Therein lies the issue market contributors face as we speak.

Nonetheless, with inflation, particularly, power prices persevering with to stress international economies, below any cheap state of affairs, the U.S. is healthier positioned for the financial dangers as we speak than Europe or Asia. For now, that’s possible inflicting capital to movement from East to West. We have seen this already in market efficiency within the final month, and it possible continues. That may function a possible offset to the “coverage disaster” right here within the U.S. How a lot of an offset stays to be seen.

Both approach, it confirms that the indecisiveness within the fairness market is completely comprehensible.

“Our prayers and ideas must be centered on the plight of the Ukrainian people who find themselves below unimaginable stress.”

POSTSCRIPT

Please enable me to take a second and remind the entire readers of an necessary difficulty. I present funding recommendation to shoppers and members of my market service. Every week I attempt to supply an funding backdrop that helps traders make their very own choices. In most of these boards, readers convey a number of conditions and variables to the desk when visiting these articles. Subsequently it’s not possible to pinpoint what could also be proper for every scenario.

In several circumstances, I can decide every shopper’s scenario/necessities and focus on points with them when wanted. That’s not possible with readers of those articles. Subsequently I’ll try to assist type an opinion with out crossing the road into particular recommendation. Please hold that in thoughts when forming your funding technique.

THANKS to the entire readers that contribute to this discussion board to make these articles a greater expertise for everybody.

Better of Luck to Everybody!

{kind=link}